In a first, 15 banks in India have come together to establish a new company which will use blockchain technology for processing inland letters of credit (LCs). The company, named Indian Banks' Blockchain Infrastructure Co Pvt Ltd (IBBIC), will have equal shareholding from 10 private sector banks, four public sector banks and one foreign bank.

This include RBL Bank, ICICI Bank, HDFC Bank, Kotak Mahindra Bank, Axis Bank, IndusInd Bank, Yes Bank, South Indian Bank, Federal Bank, IDFC First Bank, State Bank of India (SBI), Bank of Baroda (BoB), Indian Bank, Canara Bank and Standard Chartered. Each bank will invest INR 5 Crore in the company, making the total capital INR 75 Crores. As per reports, the Reserve Bank of India (RBI) has also been kept in loop on the developments and the regulator has no objection in this new venture. This is an interesting development, as Institute for Development and Research in Banking Technology (IDRBT), the technology and research arm of RBI, is also in the process of developing a model blockchain platform for banking needs.

IBBIC will use Infosys Finacle Connect platform to digitise and automate inter-organisation trade finance process on a unified distributed, trusted and shared network. With this, the banking system in India is taking a new leap in digitisation of trade finance, which has traditionally been bogged down by legacy systems and paper-driven processes. The move comes at a time when blockchain technology prototypes across the globe are fast-moving out from experimentation phase to deployment and the government is set to introduce blockchain and cryptocurrency regulations in India.

For many, the blockchain technology is still synonymous with bitcoin which came to existence in 2009. When Satoshi Nakamoto introduced bitcoin to the world, it ushered in a new era of computing – ‘the internet of trust’, a way to record transactions in a secure, immutable and transparent way. The consequences of bitcoin and the underlying technology were far-reaching, with the potential to revolutionalise everything from finance to politics. The basic concept of blockchain is to decentralise and distribute data storage so that no single entity owns, controls or manipulates data, thus providing a single source of truth.

Trade is essentially a decentralised activity and it has many intermediaries - financiers, insurers and other parties. This is a typical scenario where trust and a single source of truth are of paramount importance. The volume of documentation that happens between parties involved in establishing the ‘trust’ is humungous. The cost and time associated with preparing, transmitting and validating these documents can be counted in thousands of crores of rupees. Not to mention the losses due to instances of deceit and forgery. A blockchain, acting as a shared ledger can maintain real-time records of transactions among supply chain stakeholders, enhancing transparency in transactions and traceability of the supply chain. Creating such trusted digital data flows can reduce costs, make transactions error-free and enable faster transactions.

In India, frauds associated with LCs have been a cause of concern. It is difficult to verify the authenticity of LCs issued in physical format. In a notification by RBI to banks in 2012, issuances of LCs were made mandatorily through Structured Financing Messaging System (SFMS). SFMS is managed by Indian Financial Technology and Allied Services (IFTAS), a wholly-owned subsidiary of the Reserve Bank of India. This enhanced the verification capabilities for the banks to some extend. In 2020, a new document embedding feature was developed on SFMS by IDFC Intech, which allowed transmitting pdf documents with digital signature along with the messages, thereby enabling the parties to maintain documentary evidence for all transactions. But, the information exchange possible on the SFMS system is still limited, and does not completely eliminate the risk of duplicate

financing and fraud.

Before formation of IBBIC, Infosys Finacle had formed India Trade Connect in 2018, a blockchain-based trade network in partnership with Axis Bank, ICICI Bank, IndusInd Bank, Kotak Mahindra Bank, RBL Bank, South Indian Bank and Yes Bank. The network created was used by the banks to run a successful pilot of Finacle Trade Connect - the blockchain technology-based solution currently adopted by IBBIC. The newly formed company, with a larger participation is the positive outcome of successful pilots conducted by the Trade Connect initiative. The company is expected to launch the platform and become fully operational in less than a year. It will have an open structure, which will allow new banks to invest and participate, thereby creating strong network effects.

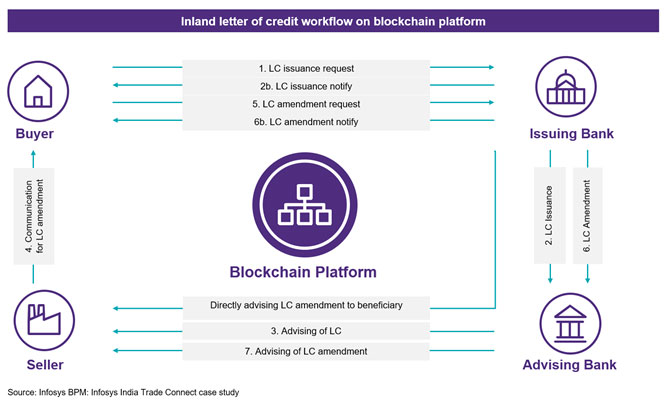

As per the details available on India Trade Connect, the blockchain network is designed to digitise trade finance business processes, including validation of ownership, certification of documents and making payments, on a distributed, trusted and shared network. The network will create new business opportunities for participating banks, while eliminating the inefficiencies in the existing trade processes and enabling everyone involved in a transaction to have a single source of the truth. The network allows for instant transfer of messages and documents between the parties involved in a completely secure manner reducing lifecycle turnaround time. The pilot run showed significant cut in cycle time for inland letter of credit; a reduction of 75% from 8-9 days to 2-3 days. Also, the digitisation reduced cost in two major areas - document courier expenses and transaction cost associated with intermediary messaging systems. As invoices and other documents were uniquely identified and stored on the blockchain, risk of duplicate financing reduced significantly. The workflow inland letter of credit issuance on the platform is illustrated as follows:

Incorporation of independent companies to run blockchain platforms is not new. Leading global blockchain trade finance platforms such as Komgo, We.trade and Contour started out as consortia of banks and other companies. All the three have moved away from that initial model and now function as separate legal entities. This is seen as essential to maintain good governance and neutrality of the platform. Independent entity can ensure that members are sharing data with a neutral entity and none of the members take undue advantage of the data available on the platform. These newly formed companies are currently running proof of concepts with the existing partners and are adding new partners at a rapid rate. Komgo, considered as world’s first blockchain-based platform for commodity trade ecosystem is backed by 15 of the world’s largest global banks, trading companies and oil giants (including BNP Paribas, Citi, ING, MUFG). Komgo supported close to USD 1 billion financing channelled by network members within one year of its public launch. Major challenge faced by all the platforms the limited network effects without numerous banks in production.

Table 1: Leading global blockchain based trade finance platforms

| Platform | Launch year | Participating institutions | Transaction volume | Technology |

| Komgo | 2019 | ABN-AMRO, BNP Paribas, Credit Agricole, Citi, Gunvor, ING, Koch Supply & Trading, Macquarie, Mercuria, MUFG Bank, Natixis, Rabobank, SGS, Shell, Société Générale | USD 1 billion | ConsenSys Quorum |

| We.Trade | 2018 | CaixaBank, Deutsche Bank, Erste Group, HSBC, KBC, Nordea, Rabobank, Santander, Société Générale, UBS and UniCredit | - | IBM Blockchain platform |

| Contour | 2020 | Bangkok Bank, BNP Paribas, CTBC Holding, HSBC, ING, SEB, and Standard Chartered, Citi, Vietnam’s HD Bank, DBS Bank, SMBC and Standard Bank | USD 1 billion | R3 Corda platform |

| Marcopolo | 2019 | BNP Paribas, Commerzbank, ING, LBBW, Anglo-Gulf Trade Bank, Standard Chartered Bank, Natixis, Bangkok Bank, SMBC, Danske Bank, NatWest, DNB, OP Financial Group, Alfa-Bank, Bradesco, BayernLB, Helaba, S-Servicepartner, Raiffeisen Bank International, Standard Bank, Credit Agricole and National Bank of Fujairah. | USD 3.3 billion | R3 Corda platform |

Meanwhile, private blockchains owned by Chinese banks have clocked large transaction volumes. Recently, an Ethereum-based private blockchain platform developed by China Construction Bank called BCTrade clocked transactions worth USD 50 billion, thereby making it the largest trade finance platform in the world. The bank runs the platform through its subsidiary - Jianxin Financial Services. Industrial and Commercial Bank of China, world’s largest bank by assets, also owns a blockchain trade finance platform which has clocked transactions worth USD 6.5 billion so far.

Blockchain technology is still considered to be in its infancy and is often compared to the internet in early 90’s. The applications are not limited to trade finance or cross border payments. Several banking consortiums have emerged worldwide in the last few years in collaboration with technology providers to advance the use of blockchain and find new application areas in financial services. The regulatory landscape is also evolving taking cognisance of the fast-paced developments.

IBBIC, the newly incorporated entity with stakes from top banks in the country is a potential game-changer for BFSI sector in India. Though the scope is currently limited to addressing issues in trade financing, the company can also bring focus to research, exploration and implementation of new blockchain solutions and keep the financial services sector in India at the leading edge of innovation. The company can also collaborate with GoI and regulators to shape regulations in a meaningful way so that the full potential of blockchain technology is unlocked and an enabling environment is created for new advances.